Why Indian Family Offices are Abandoning Domestic Real Estate for the ‘Sovereign Yield’

The 2% Paradox

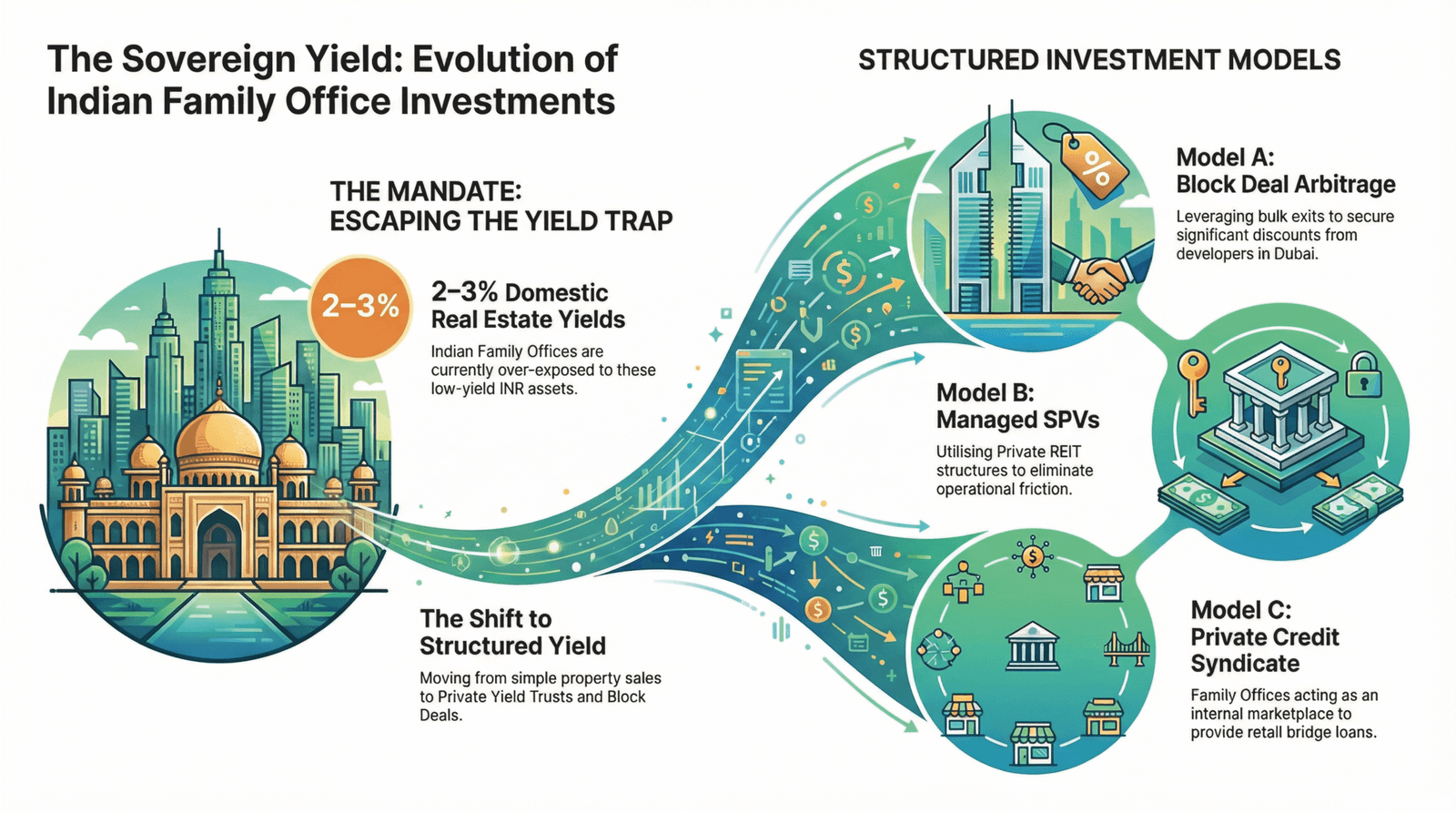

For the modern Indian Family Office, the romance of domestic real estate has curdled into a mathematical trap. Historically, the “landlord” status in Mumbai or Delhi was a badge of prestige, but in today’s inflationary environment, it has become a liability. We call this the 2% Paradox : the frustration of holding high-value, illiquid assets that yield a meager 2–3% in a currency—the Indian Rupee (INR)—that remains exposed to sovereign volatility and domestic inflation.The days of chasing door keys in Mumbai or Bangalore are over; they’ve been replaced by the pursuit of structured entry points in global hubs. This isn’t just a change in geography; it is a fundamental shift in DNA. Sophisticated capital is no longer “buying buildings”; it is migrating toward “Private Yield Trusts” that offer hard-currency protection. The goal is no longer to own the roof, but to own the yield.

Takeaway 1: The Death of the ‘Property’ Mindset

The transition from a traditional landlord to an institutional strategist requires a total abandonment of the “bricks and mortar” ego. Indian wealth is professionalizing at an unprecedented rate, moving away from the operational headaches of individual asset management toward structured vehicles.In this new era, the transaction is no longer the end goal—the structure is. Family Offices are prioritizing “Off-Market Block Deals” and “Private Yield Trusts” that allow them to bypass the inefficiencies of the retail market.”We do not sell ‘properties’; we structure ‘Private Yield Trusts’ and ‘Off-Market Block Deals’.”By adopting this institutional-grade mindset, these offices are effectively decoupling their wealth from the stagnant yields of the domestic market and re-anchoring it in jurisdictions that offer superior risk-adjusted returns.

Takeaway 2: Exploiting the ‘Block Deal’ Arbitrage (Model A)

In global liquidity hubs like Dubai, the real profit is made at the entry, not the exit. The “Block Deal” arbitrage model exploits a specific developer pain point: the need for rapid capital recycling. When a developer seeks a bulk exit to de-risk a project, they offer significant discounts—often as high as 20%—to a single institutional buyer who can close quickly.For an Indian Family Office, the math is transformative. A 20% discount on a bulk acquisition is the equivalent of capturing ten years of domestic Indian rental yield on Day 1. This is the essence of the arbitrage—securing a decade’s worth of profit through smart capital deployment before the first tenant even moves in. It turns real estate into a high-margin financial instrument rather than a slow-burning utility.

Takeaway 3: Solving Friction via Managed SPVs (Model B)

Cross-border investing is traditionally plagued by “friction”—the administrative, tax, and operational burdens that erode net returns. To combat this, the “Managed SPV” or “Private REIT” has become the preferred vehicle for Indian capital. This model professionalizes the ownership experience, allowing the Family Office to enjoy the rewards of global real estate without the “leaky toilet” syndrome of direct management.By utilizing this professionalized structure, investors gain three distinct institutional efficiencies:

- Tax and Regulatory Shielding: The SPV acts as a protective layer, optimizing cross-border tax liabilities and ensuring compliance with both Indian and international regulatory frameworks.

- Operational Decoupling: Professional management removes the Family Office from the day-to-day friction of tenant disputes, maintenance, and rent collection, converting an active burden into a passive income stream.

- Liquidity through Unitization: Unlike a physical floor of a building, which is notoriously difficult to sell partially, a Private REIT structure allows the family to exit or rebalance portions of their holding with institutional ease.

Takeaway 4: The Internal Marketplace (Model C)

The final evolution of the sophisticated Family Office is the move from “Landlord” to “Lender.” Through the “Private Credit Syndicate” model, Family Offices are no longer competing with retail buyers for assets; they are financing them. By providing bridge loans to retail purchasers, the Family Office moves up the capital stack, capturing a high-interest spread without the friction of asset maintenance.This is where the concept of the Sovereign Yield truly matures. By lending in a USD-pegged jurisdiction like Dubai (where the Dirham is fixed to the Dollar), the Family Office secures a hard-currency yield that far outperforms the sovereign-risk-adjusted returns of Indian real estate. They are essentially creating an internal marketplace—capturing the spread, avoiding the operational overhead of ownership, and shielding their wealth from the depreciation of the Rupee.

Conclusion: The Future of the Sovereign Yield

The mass migration of Indian private wealth into global structured real estate is more than a trend; it is a professionalization of the Indian balance sheet. By abandoning the low-yield traps of the domestic market for Block Deal arbitrage, Managed SPVs, and Private Credit syndicates, Family Offices are securing their legacy in hard-currency jurisdictions.The global flow of Indian capital is no longer looking for a place to sit; it is looking for institutional-grade structuring that provides a Sovereign Yield. The gap between those who own “properties” and those who own “structures” is widening.Is your own portfolio still stuck in the 2% low-yield trap, or are you ready to transition to institutional-grade structuring?

Recent Posts

Why Indian Family Offices are Abandoning Domestic Real Estate for the ‘Sovereign Yield’

The 13% Arbitrage: Why Indian Developers are Reimagining Dubai as a ‘Treasury Tool’