Beyond the Bull Run: How Global Arbitrage is Rewriting the Indian Trader’s Playbook

Introduction: The High Cost of Winning

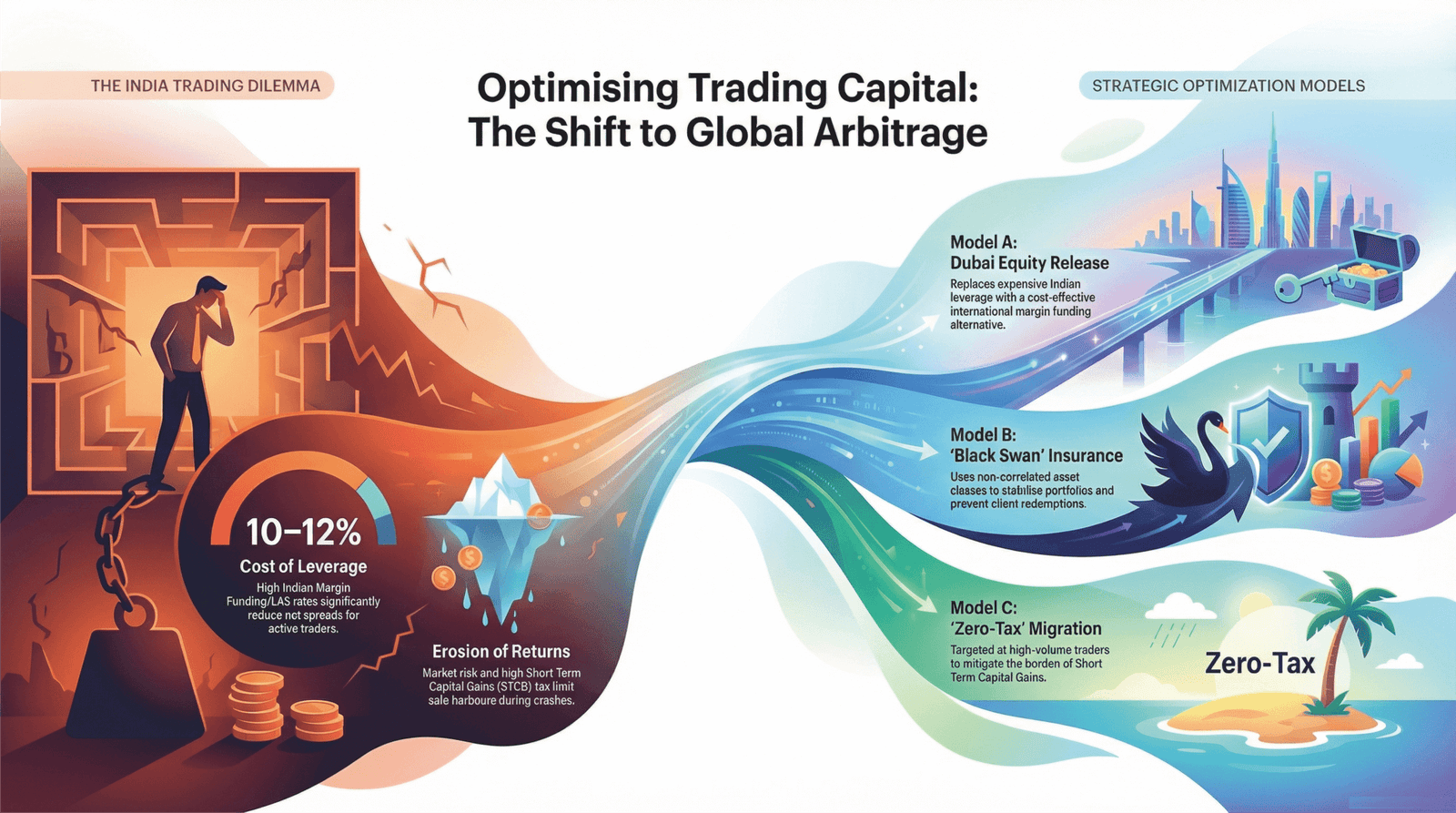

In the upper echelons of active trading, we often witness a structural failure of the local landscape known as the “Trader’s Dilemma.” While the pursuit of Alpha—generating excess returns—is the primary objective, those returns are frequently cannibalized by two systemic forces: high local taxation and the exorbitant cost of leverage.For the Indian trader, the struggle is not merely against market volatility (Beta), but against a domestic environment that imposes a massive hurdle rate on every position. During a bull run, impressive INR profits may accrue on paper, but the reality of net capital growth is often much bleaker. True capital optimization requires a shift in perspective, moving beyond local market mastery into the realm of Strategic Arbitrage and Global Capital Optimization.

Model A: The Margin Funding Alternative (The Ultimate Carry Trade)

The most immediate drain on a trader’s net spread is the inefficiency of the Indian Margin Funding and Loan Against Shares (LAS) ecosystem. When you rely on local leverage, you are effectively accepting a tax on your performance before you even enter the market.1. Your Leverage is Leaking AlphaIn the Indian context, the cost of securing leverage acts as a persistent headwind against yield compression. By utilizing local margin funding, a substantial portion of your potential alpha is redirected toward interest payments, significantly raising your break-even point.”The Cost of Leverage (Margin Funding/LAS) in India is high (10-12%), eating into your net spread.”The strategic response is to engage in a “Carry Trade” via Dubai Equity Release. This is not a simple loan replacement; it is jurisdictional arbitrage. By borrowing in a global, lower-interest environment to fund higher-yielding Indian assets, a trader can bypass the 12% local hurdle rate. This pivot immediately optimizes the cost of capital, allowing the trader to retain a much larger portion of the net spread.

Model B: The ‘Black Swan’ Insurance – Solving the Redemption Crisis

For Portfolio Managers (PMs), the ultimate threat to business continuity is not a temporary market dip, but the “Redemption Crisis.” When the market enters a significant drawdown, psychological pressure forces clients to withdraw capital, often compelling PMs to liquidate undervalued positions at the worst possible moment.2. Stabilizing the Portfolio with Non-Correlated AssetsTo maintain institutional-grade stability, one must introduce a non-correlated asset class into the mix. This serves as a “Liquidity Bridge”—a strategic buffer that does not move in tandem with standard Indian bull and bear cycles.The integration of this model provides:

- Drawdown Mitigation: Reducing the depth of portfolio declines during market crashes.

- Preservation of Alpha: Preventing the forced liquidation of core assets, ensuring that long-term compounding remains uninterrupted.

- Business Continuity: Providing a “Safe Harbour” that preserves client confidence and stabilizes the fund’s AUM during periods of high volatility.

Model C: The ‘Zero-Tax’ Migration – The Math of Global Arbitrage

For high-volume traders, Short Term Capital Gains (STCG) is more than just a tax; it is a critical leak in the compounding engine. As trading volume scales, the fiscal friction of the Indian tax regime becomes a mathematical barrier to reaching the next tier of wealth.3. The Math of MigrationWhen the tax environment begins to dictate your exit strategy or position sizing, you have outgrown the local infrastructure. In this framework, migration is viewed through the lens of capital efficiency.For high-volume traders paying significant Short Term Capital Gains (STCG) in India, the transition to a “Zero-Tax” environment is the ultimate strategic move.The “Math of Migration” is undeniable. By shifting the center of operations to a more favorable jurisdiction, a high-volume trader converts what was previously a 15-20% tax expense back into working capital. This capital stays in the pool, compounding year-over-year, and drastically accelerating the growth trajectory of the primary fund.

Conclusion: The New Era of Capital Mobility

The modern trader is no longer a prisoner of local geography or localized interest rates. The “Strategic Arbitrage and Global Capital Optimization” framework proves that the tools to overcome the Trader’s Dilemma are now within reach.Whether it is replacing double-digit interest rates with global equity release, insulating a portfolio against black swan events through non-correlated assets, or plugging the tax leak through migration, the objective remains the same: total capital efficiency.The era of accepting local inefficiencies as an inevitable cost of trading is over. As capital becomes increasingly mobile, every serious market participant must ask: Is your portfolio’s growth limited by your trading strategy, or is it simply limited by your geography?

Recent Posts

Why Indian Family Offices are Abandoning Domestic Real Estate for the ‘Sovereign Yield’

The 13% Arbitrage: Why Indian Developers are Reimagining Dubai as a ‘Treasury Tool’